FOR PROFESSIONAL INVESTORS AND/OR QUALIFIED INVESTORS AND/OR FINANCIAL INTERMEDIARIES ONLY. NOT FOR USE WITH OR BY PRIVATE INVESTORS. CAPITAL AT RISK. All financial investments involve taking risk and the value of your investment may go down as well as up. This means your investment is not guaranteed and you may not get back as much as you put in. Any income from the investment is also likely to vary and cannot be guaranteed.

Every investor with a passing knowledge of equities is likely to have heard of the small-cap effect: over the medium to long term, the returns from owning smaller companies have far exceeded those derived from owning larger ones. This is because smaller companies have more ‘white space’ to expand into, benefit from scale economies as they grow and tend to be run by management teams with more ‘skin in the game’ in terms of share ownership.

Data from Deutsche Numis shows that if somebody invested £1,000 in UK small caps on behalf of a new-born baby in 1955, by the time it retired in 2022 at the age of 67, this amount would have grown to £9m (assuming all dividends were reinvested). Had they invested the same amount in UK large caps instead, the £1,000 still would have grown substantially, but to £1m rather than £9m.

Yet ever since the UK voted to leave the European Union in June 2016, the small-cap effect seems to have ground to a halt.

Data from Bloomberg shows the renamed Deutsche Numis Smaller Companies (ex ICs) index made a total return of 47% between the date of the referendum result and the end of March 2024 – well below the 65% made by the FTSE All-Share.

As international investors have shunned the UK and multiples have fallen, there has been a waning appetite among smaller companies to list on the domestic market. With M&A activity at heightened levels, analysis from Peel Hunt shows the number of FTSE Smallcap constituents fell from 160 at the end of 2018 to 114 at the end of 2023. If the decline continues at its current rate, the FTSE Smallcap index will cease to exist by 2028.

It looks like the direction of travel for UK smaller companies is only going one way, right? We disagree.

It is difficult to find much evidence that Brexit has affected listed small caps’ day-to-day operations. We have 300 to 500 meetings a year with company management teams and few mention it as an issue.

Brexit’s impact on business fundamentals

It is true that Brexit has caused small caps to de-rate. Investors started pulling money out of the UK equity market on the day of the referendum result and the direction of flows is yet to reverse.

However, it is perhaps worth asking who the marginal seller is from here? Domestic pension funds are now all but out of the UK market. Momentum investors would have sold out long ago. International investors that remain have already weathered the threat of Jeremy Corbyn and the debacle surrounding Liz Truss. One would imagine they are here to stay.

What of fundamentals? It is difficult to find much evidence that Brexit has affected listed small caps’ day-to-day operations. We have 300 to 500 meetings a year with company management teams and few mention it as an issue.

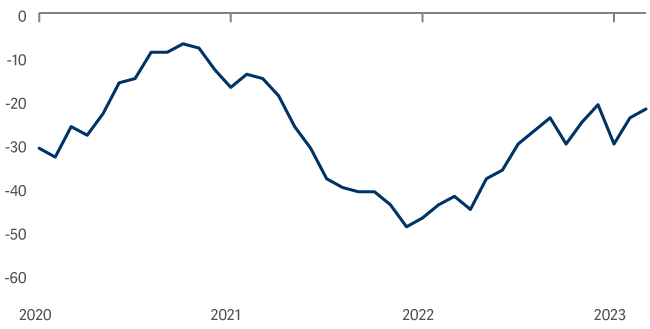

At the same time, the UK economy, to which small caps have a higher exposure than their larger counterparts, is improving. Consumer confidence and the Asda Income Tracker have both been rising for several months now. Government debt levels are low relative to other G7 countries. And, for all the scepticism towards the UK, its PMI is currently top of the developed economy league table.

Year-on-year change in Asda income tracker (£)

![]()

Source: Asda as at 29 February 2024

UK consumer confidence is recovering (UK Consumer Confidence Index)

Source: Lazarus as at 31 March 2024

Outperformance not dependent on a re-rating

You are probably sick of hearing the argument that UK small caps are cheap. Yet even if there isn’t a re-rating, the valuation differential should be enough for UK small caps to outperform from here.

Take two theoretical companies: both grow at 7% a year and pay out 50% of their income. Company A trades on a P/E of 15x and Company B trades on 10x. Over a 10-year period, without a re-rating of Company B, it will make 17 percentage points more than Company A. Why? Because the benefit of reinvesting dividends at a lower valuation compounds up over time.

In addition, many UK small caps are turning depressed valuations to their advantage through the use of share buybacks. Eleven of our portfolio holdings in the Artemis UK Smaller Companies Fund bought back their own shares in 2023, with six more already announcing plans to do so this year1.

When companies buy back shares, it increases potential dividends and earnings per share (EPS) for remaining investors. The lower the valuation, the greater the impact. As an example, we recently spoke to Simon Emeny, the chief executive of pub operator Fuller’s, who pointed out the company would have to spend twice as much buying a new pub as it would by buying back its own shares (effectively buying its own pubs at a discount).

And, as mentioned, small caps remain the target of heightened M&A activity: 28 of our fund’s holdings have been taken over since 2019, at an average premium of 50%. To Peel Hunt’s point about the FTSE Smallcap index eventually ceasing to exist: while it now only numbers 114 companies, there are more than 1,000 to choose from in the Deutsche Numis Smaller Companies index, including those quoted on the AIM market.

We believe a combination of low starting valuations, the growing use of buybacks and continued M&A activity should be enough to drive outperformance in the coming years. But if we are right, another factor is likely to come into play.

The point of maximum pessimism

The steady de-rating of the UK small-cap sector is like a piece of elastic that has become more and more stretched the further away it gets from the historical average. When small caps start to outperform, investors that have reallocated to other areas will be harmed by their underweight and will likely re-evaluate their exposure. At this point, greed will come back into the market and the elastic that has been stretched over the past eight years will suddenly snap back.

Just think, the small-cap effect doesn’t arise from consistent year-on-year outperformance, but from periods of extremely large gains. For example, the Numis Smaller Companies (ex ICs) index made 73% across 2003 and 2004, and 107% across 2009 and 2010.

You may have noticed that both of these two-year periods came after the bursting of the dotcom bubble and the end of the Global Financial Crisis, when the point of maximum pessimism had been reached. So are we close to the point of maximum pessimism right now?

We’ll let you be the judge of that.

1 Source: Artemis as at 1 May 2024

FOR PROFESSIONAL INVESTORS AND/OR QUALIFIED INVESTORS AND/OR FINANCIAL INTERMEDIARIES ONLY. NOT FOR USE WITH OR BY PRIVATE INVESTORS.