14 Sep 2021

The stockmarket is prone to bubbles and crashes. Craig Bonthron explains how the Artemis impact equities team seeks to reduce its exposure to those crises by seeking idiosyncratic sources of return.

FOR PROFESSIONAL AND/OR QUALIFIED INVESTORS ONLY. NOT FOR USE WITH OR BY PRIVATE INVESTORS. CAPITAL AT RISK. All financial investments involve taking risk which means investors may not get back the amount initially invested.

“Economists later figured that, on the basis of the market’s historical volatility, had the market been open every day since the creation of the Universe, the odds would still have been against its falling that much in a single day. In fact, had the life of the Universe been repeated one billion times, such a crash would still have been theoretically ‘unlikely’.”

Roger Lowenstein When Genius Failed: The Rise and Fall of Long Term Capital Management

If the efficient market hypothesis held, then none of the bubbles and crashes that have punctuated the history of financial markets would have occurred. So if markets are not efficient, then what are they?

The best answer to emerge from academia over the last 30 years appears to be the theory of ‘complex adaptive systems’ (CAS), “a system that is complex in that it is a dynamic network of interactions, but the behaviour of the ensemble may not be predictable according to the behaviour of the components.” (Wikipedia).

The theory, originally developed to aid understanding of biological ecosystems, allows for a level of efficiency that is not bound by the strictures of normal distributions or by the notion of emotionless ‘rational actors’. Inefficiencies, bubbles, asymmetric risk, skewed distributions (fat tails, long tails) can all occur in a complex adaptive system – just as they do in real life.

Moreover, it also allows for the idea that fragility can build unseen within markets. Consider a pile of sand which grows as individual grains are added from above. As the pile grows, hidden ‘fingers of instability’ are created. Instability is built upon instability and these can persist for an unpredictable period. At a certain point, however, a critical state is reached: the addition of a single grain of sand triggers a collapse in the structure of the entire pile. The longer the instability persists, the bigger the eventual landslide.

Within the complex adaptive system of the stockmarket, bubbles and crashes are a crisis of un-differentiation. These are events in which we see extreme (short-term) homogeneity of movements, either up or down. Instabilities that have been created slowly, whether through price-insensitive passive or rules-based investment strategies – or through human psychology (behavioural finance has conclusively proven that we are less rational than we might like to think) are suddenly revealed.

Why does this matter? It matters because by acknowledging the existence of these instabilities we can consciously attempt to mitigate their impact. First, we can recognise these instances of un-differentiation are more likely to occur in some markets and asset classes than in others.

The second, allied point is that we recognise that inefficiencies exist and deliberately seek to exploit them. For skill to be rewarded in our complex adaptive system - the global equity market - we need to find a high number of less-correlated assets to select from; we need to look where there is greater differentiation. So we are deliberately targeting those areas of the market that have a high dispersion of returns (i.e. differentiation) and which offer us fertile hunting grounds.

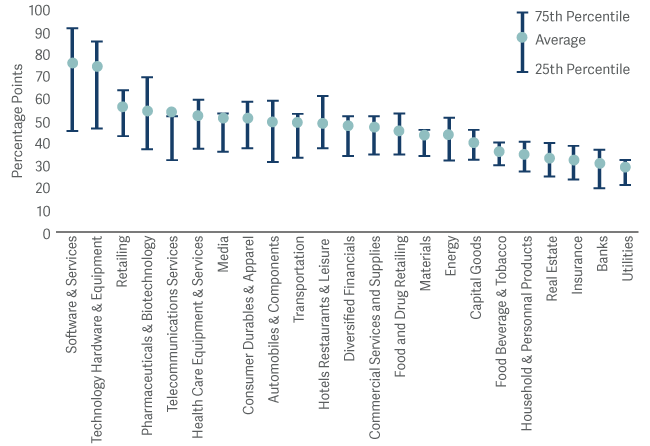

Some sectors offer far greater dispersion – and so more opportunity to demonstrate stockpicking skill – than others. Between 1985 and 2019, technology industries offered the highest dispersion of returns; real estate and utilities among the lowest.

“When the distribution is wide, there is a lot of positive and negative alpha. That’s good news if you are skilful, because it’s easy to find a loser that allows you to win. When the distribution is narrow, there is not a lot of positive alpha, and it’s hard to separate the skilled from the unskilled [manager]… The relationship is quite clear. More dispersion tends to spell more opportunity. Talented managers need dispersion in order to ply their skill.”

Michael J. Mauboussin, Dispersion and Alpha Conversion (April 2020)

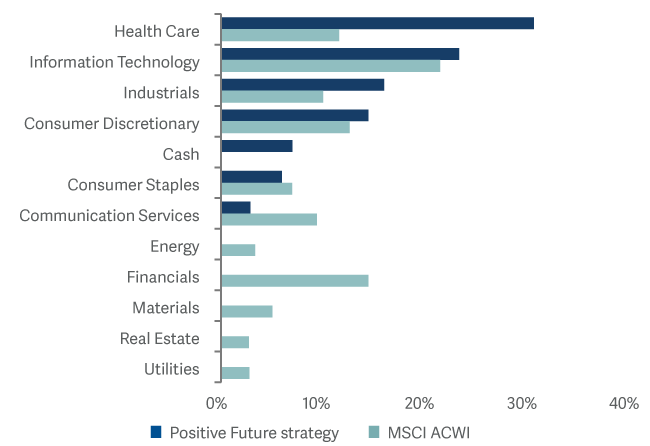

We focus on areas of high dispersion and breadth because our goal is to find significant idiosyncratic returns and so take less systemic risk. We consciously, deliberately operate outside our comfort zone and embrace the unorthodox. Information about the types of stock we invest in is scarcer than it is for mega-caps; and passive and quant investors are less present in our corner of the market. Even many active managers find our companies uncomfortable to own due to their volatility.

We focus on sectors where the dispersion of returns is highest.

The discomfort we feel is the price we pay for holding a differentiated portfolio of investments that not only have a positive impact (and, we hope, superior long-term returns), but which also have a lower correlation to the systemic risks – the fingers of instability - building unseen in the wider market. The market may suffer further crises of un-differentiation this year; it doesn’t necessarily mean our portfolio will.

To find out more about Artemis Fund Managers visit www.artemisfunds.com.

FOR PROFESSIONAL AND/OR QUALIFIED INVESTORS ONLY. NOT FOR USE WITH OR BY PRIVATE INVESTORS. CAPITAL AT RISK. All financial investments involve taking risk which means investors may not get back the amount initially invested.

Any research and analysis in this communication has been obtained by Artemis for its own use. Although this communication is based on sources of information that Artemis believes to be reliable, no guarantee is given as to its accuracy or completeness.

Any forward-looking statements are based on Artemis’ current expectations and projections and are subject to change without notice.

Issued by Artemis Fund Managers Ltd which is authorised and regulated by the Financial Conduct Authority.