07 Jun 2023

The interlinked nature of multiple global events – known as the polycrisis – can create challenges and opportunities for investors. Sunil Krishnan explores the potential winners, losers and areas of change.

Read this article to understand:

Coming hot on the heels of the COVID-19 pandemic, Russia’s invasion of Ukraine in February 2022 triggered a cascade of inflationary shocks, particularly to energy prices. Since then, central banks have aggressively raised interest rates, fuelling recession fears. These may be tempered by China’s belated reopening from COVID-19, which will, however, add to demand pressures on energy and commodities, potentially pushing prices higher again. All this is unfolding against the backdrop of the global climate emergency.

Commentators have dubbed this series of multiple interlinked global challenges the “polycrisis”.1 The interactions between the various factors make it difficult to assess its impact on the economy, and subsequently portfolios. One way to approach this is to break it down thematically between potential losers and winners from the polycrisis, and areas where it is too early to tell but we know there will be change.

The UK economy has been losing out in the polycrisis. It has suffered acutely from the energy crisis because it is dependent on gas imports but does not have energy resilience. It has insufficient gas storage capacity and has not subsidised energy prices in the same way as other European countries, meaning its economy has been at the mercy of spot price increases.2

The UK economy has suffered acutely from the energy crisis because it is dependent on gas imports

In 2022, this came on top of other drivers of inflation, low productivity and complicating factors like governmental instability and Brexit. Although market confidence has since been restored, the Bank of England is raising interest rates, adding to the confluence of issues weighing on UK growth more than in any other developed economy.3

As far as portfolio impact, we prefer foreign currencies to sterling but see a positive opportunity in gilts relative to other bond markets. Because of the UK’s ongoing limits to growth, the Bank of England will likely have to stop raising interest rates sooner than other countries. That would give the gilt market an opportunity to outperform.

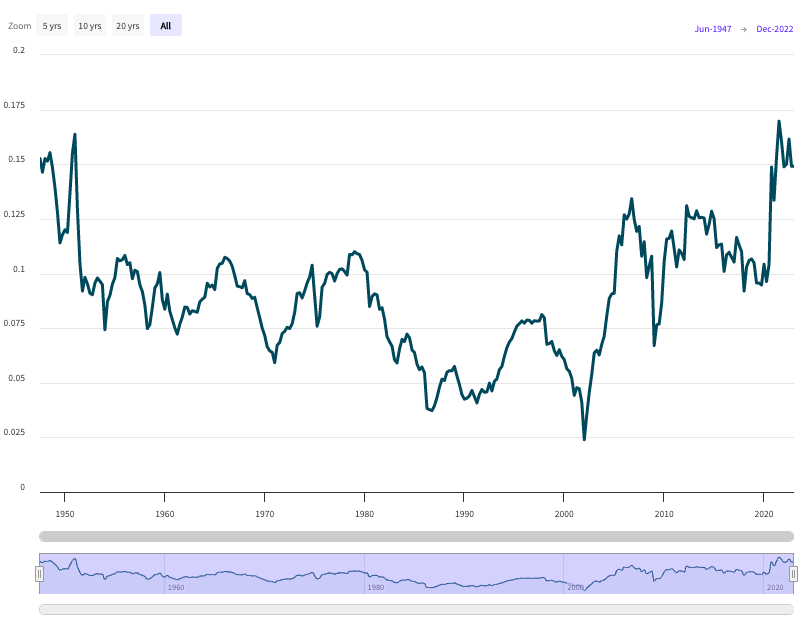

After a strong start to 2023, there are challenges ahead for global equities. This year will probably be better for GDP than expected at the height of the energy crisis last September. But revenue – and therefore earnings – growth will not be stellar, especially as central banks will continue tightening monetary policy until they are comfortable inflation has been dealt with, even if consumer demand slows further.

It will be even more difficult to maintain profit margins. They are high, particularly in the US, but this could reverse as slower costs like wages continue to rise but can no longer be passed through fully to consumers.

Figure 1: US corporate profit margins

Source: Bloomberg. Data as of December 31, 2022

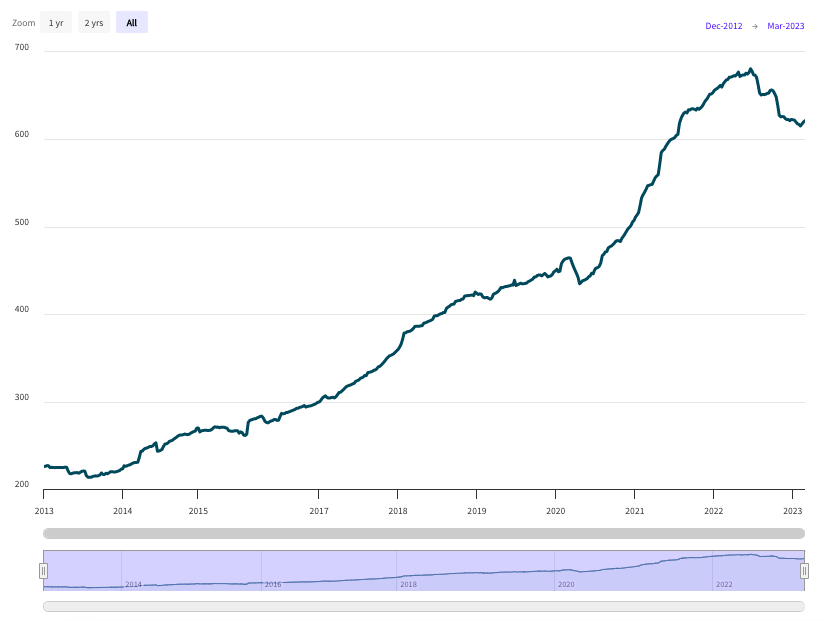

In companies where investors had projected strong rates of compounded growth, high equity valuations look questionable. The biggest tech names are the obvious example, as their latest reporting and guidance does not fit with sustained above-market earnings growth. At a time when yields on assets like bonds and cash have improved, that will put pressure on richly valued stocks.

Figure 2: Nasdaq 100 earnings estimates +2 years

Source: Bloomberg. Data as of February 28, 2023

Because we do not have visibility on how far earnings may deteriorate, we have reduced our equity exposure only moderately versus long-term strategic weights.

The polycrisis is creating potential winners within equities, such as healthcare, energy and raw materials. We have added a position in European healthcare to complement our US holding and increased our exposure to commodity producers, adding a position in European materials to our European energy holding.

As the Financial Times’s Simon Kuper recently wrote, the polycrisis is enabling poly-innovation. This is particularly true in pharmaceuticals.4

A rare positive outcome of the COVID-19 pandemic was the speed of adoption of mRNA vaccines

A rare positive outcome of the COVID-19 pandemic was the speed of adoption of mRNA vaccines – the new type of vaccines used by Pfizer-BioNTech and Moderna against COVID-19 that uses messenger RNA (mRNA) to teach cells to make a protein triggering an immune response to a chosen virus.5

In a different era, this technology would have taken decades to be approved and embraced. Instead, not only did it change the outcome of the pandemic, it is also being used in applications like antimalarial vaccines and could eventually address some of humanity’s longstanding health challenges.

Clinical trials also show momentum in the industry. In 2022, the global success rate for pivotal trials was 71 per cent globally, above the five-year ex-COVID average of 62 per cent. In the US, it was 85 per cent.6

Moreover, other technologies such as big data and modelling are now being put to better use in clinical trials, to improve understanding of health conditions and potential responses to treatments.7

The other potential polycrisis winner is European energy, both in terms of energy security from a geopolitical standpoint and the net-zero transition.

European energy companies must be part of the solution on both fronts and are already substantial investors in renewable and low-carbon energy. A few years ago, the question was whether they could generate enough cashflows to return money to shareholders as well as investing in the transition. Today, they are awash with cash and it is easy to see how they can achieve both. We also find them more attractive than their US competitors.

1.5trn Cash reserves among energy companies to allocate to low-carbon activities

Analysis by Deloitte last summer suggests that, even as companies strive to meet their primary obligations to their shareholders, they are estimated to still have cash reserves of US$1.5 trillion between 2022 and 2030 to allocate to low-carbon activities.8

TotalEnergies has the highest percentage among peers of capital spending dedicated to low-carbon initiatives, at 25 per cent. It reported a 44 per cent effective tax rate in the third quarter of 2022, up from 39 per cent in the previous quarter, largely due to the UK energy profit levy and a projected €1 billion EU solidarity tax.

Despite this, the company is still aiming for double-digit profitability in its low-carbon segment as it continues to grow its LNG strategy with a stake in the North Field South LNG project in Qatar. Meanwhile, additional costs due to inflation and higher interest rates will be passed on to the customers in power-purchase agreements, so the company can stay on course for its goal.9

In addition, electrification will be an essential part of the energy transition. That will generate substantial demand for minerals and metals like copper and aluminium, which is why we have added an allocation to the resources sector.10

In contrast to the end of the last commodity super-cycle in 2006-2007, both energy and mining have been cautious in their capital investments. That reinforces their attractiveness, as it means we are a long way from a risk of oversupply in these core resources, particularly when we also consider China’s reopening.

Figure 3: Inventories of major metals (kilotons)

.png)

Source: Bloomberg. Data as of February 28, 2023

Xi Jinping’s recent speech to the Central Economic Working Conference underscores a commitment not just to economic growth, but to stimulating demand.11 This is supportive for China's domestic economy, but even more so for global resources demand.

Responses to European energy security concerns, the climate emergency and China’s post-COVID economic challenges are creating favourable conditions for the extractive industries.

The last theme is an area where we know things will look different, but it is too early to identify the winners and losers. That is Japan and the move towards changes in its monetary policy regime.

Seemingly unshakeable positions are now open to discussion

For several years, Japan has targeted a zero-interest rate by controlling its yield curve. We also note the Bank of Japan’s (BoJ) comments in December that its adjustments, which moved the market, were purely technical and designed to make yield-curve control work better. Yet these seemingly unshakeable positions are now open to discussion.12

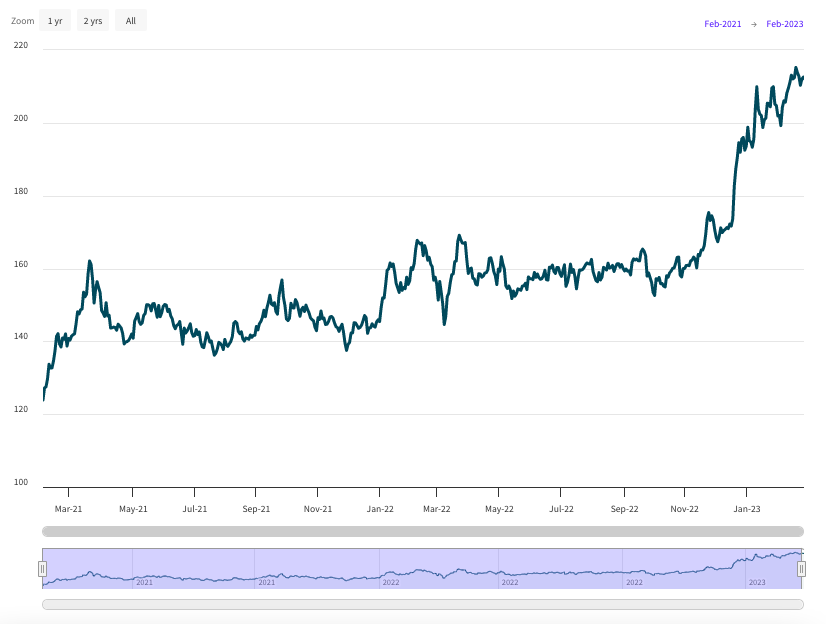

Not only is Japanese headline inflation the highest in many years, but some of the more sustainable drivers of inflation, particularly wages, are also rising. The recent “shunto” (spring wage bargaining) round is coming in a little stronger than investors expected. Rather than wait for the next agreement, some companies have even increased wages over and above what had been previously agreed.13

Figure 4: Japan CPI inflation (year-on-year, per cent)

.png)

Source: Bloomberg. Data as of February 28, 2023

It increasingly seems Japan has succeeded in its objective to return to normal inflation levels. That raises questions of domestic economics and politics. Our understanding is the Ministry of Finance is not enamoured of yield-curve control, and would favour a gradual return to market-based pricing of interest rates.

Japan’s exit from yield-curve control is just a question of timing

Despite the debate around the nomination of the next BoJ governor, we regard the desire to move to a gradual exit as fairly mainstream among BoJ officials. The chosen candidate, Kazuo Ueda, is seen as neither extremely hawkish nor dovish, which suggests he will not throw the exit into question, even if he prefers to take a careful approach.

Therefore, the exit from yield-curve control is just a question of timing. As long-term investors, our job is to not get too caught up in short-term volatility but see the bigger picture. This is a move towards higher interest rates across the curve. That would be supportive of a stronger currency and financial investment coming back into Japan, so we are backing these themes in portfolios through underweight positions in Japanese government bonds and long positions in Japanese yen.

Other consequences of Japan’s policy normalisation are not totally clear. For example, it could be great news for the Japanese banking sector. After the BoJ’s tweak to yield-curve control in December, which many investors took to be the beginning of the end, Japanese banks did well because higher interest rates would allow them to finally be more profitable. These banks could be attractive for investors, as long as they avoid bad loans if companies can't make payments because of higher rates.

Figure 5: Japan Topix banks’ index price

Source: Bloomberg. Data as of March 1, 2023

Another, potentially even bigger, consequence is we can only guess at the amount of overseas bonds held by Japanese investors. If Japanese government bonds begin to offer much higher interest rates, Japanese investors might switch, creating a lot of selling pressure in overseas bonds.

The consequences of the polycrisis are complex and far-reaching

In terms of the global rise in yields that began 18 months ago, the last shoe could drop when Japanese investors start selling their holdings of US Treasuries. This is not quantifiable ahead of time, but is a risk we continue to monitor.

The consequences of the polycrisis are complex and far-reaching; we have not seen the end, and investors should remain alert to events. But it has also stimulated innovation and created opportunities.

1 Jonathan Derbyshire, “Year in a word: Polycrisis”, Financial Times, January 1, 2023

2 “Gas versus renewables: Does natural gas have a future?”, Aviva Investors, March 2023

6 “Sector review: Major pharma 2023”, Credit Suisse equity research, January 6, 2023

9 “Third Quarter 2022 Results”, TotalEnergies, October 27, 2022

10 “The economics of renewables: Challenges and solutions”, Aviva Investors, February 10, 2023

13 “2023 "Shunto" wage talks kick off in Japan amid surging prices”, Nippon Communications Foundation, January 23, 2023

THIS IS A MARKETING COMMUNICATION

Except where stated as otherwise, the source of all information is Aviva Investors Global Services Limited (AIGSL). Unless stated otherwise any views and opinions are those of Aviva Investors. They should not be viewed as indicating any guarantee of return from an investment managed by Aviva Investors nor as advice of any nature. Information contained herein has been obtained from sources believed to be reliable, but has not been independently verified by Aviva Investors and is not guaranteed to be accurate. Past performance is not a guide to the future. The value of an investment and any income from it may go down as well as up and the investor may not get back the original amount invested. Nothing in this material, including any references to specific securities, assets classes and financial markets is intended to or should be construed as advice or recommendations of any nature. Some data shown are hypothetical or projected and may not come to pass as stated due to changes in market conditions and are not guarantees of future outcomes. This material is not a recommendation to sell or purchase any investment.

The information contained herein is for general guidance only. It is the responsibility of any person or persons in possession of this information to inform themselves of, and to observe, all applicable laws and regulations of any relevant jurisdiction. The information contained herein does not constitute an offer or solicitation to any person in any jurisdiction in which such offer or solicitation is not authorised or to any person to whom it would be unlawful to make such offer or solicitation.

In Europe, this document is issued by Aviva Investors Luxembourg S.A. Registered Office: 2 rue du Fort Bourbon, 1st Floor, 1249 Luxembourg. Supervised by Commission de Surveillance du Secteur Financier. An Aviva company. In the UK, this document is by Aviva Investors Global Services Limited. Registered in England No. 1151805. Registered Office: St Helens, 1 Undershaft, London EC3P 3DQ. Authorised and regulated by the Financial Conduct Authority. Firm Reference No. 119178. In Switzerland, this document is issued by Aviva Investors Schweiz GmbH.

In Singapore, this material is being circulated by way of an arrangement with Aviva Investors Asia Pte. Limited (AIAPL) for distribution to institutional investors only. Please note that AIAPL does not provide any independent research or analysis in the substance or preparation of this material. Recipients of this material are to contact AIAPL in respect of any matters arising from, or in connection with, this material. AIAPL, a company incorporated under the laws of Singapore with registration number 200813519W, holds a valid Capital Markets Services Licence to carry out fund management activities issued under the Securities and Futures Act (Singapore Statute Cap. 289) and Asian Exempt Financial Adviser for the purposes of the Financial Advisers Act (Singapore Statute Cap.110). Registered Office: 1 Raffles Quay, #27-13 South Tower, Singapore 048583.

In Australia, this material is being circulated by way of an arrangement with Aviva Investors Pacific Pty Ltd (AIPPL) for distribution to wholesale investors only. Please note that AIPPL does not provide any independent research or analysis in the substance or preparation of this material. Recipients of this material are to contact AIPPL in respect of any matters arising from, or in connection with, this material. AIPPL, a company incorporated under the laws of Australia with Australian Business No. 87 153 200 278 and Australian Company No. 153 200 278, holds an Australian Financial Services License (AFSL 411458) issued by the Australian Securities and Investments Commission. Business address: Level 27, 101 Collins Street, Melbourne, VIC 3000, Australia.

The name “Aviva Investors” as used in this material refers to the global organization of affiliated asset management businesses operating under the Aviva Investors name. Each Aviva investors’ affiliate is a subsidiary of Aviva plc, a publicly- traded multi-national financial services company headquartered in the United Kingdom.

Aviva Investors Canada, Inc. (“AIC”) is located in Toronto and is based within the North American region of the global organization of affiliated asset management businesses operating under the Aviva Investors name. AIC is registered with the Ontario Securities Commission as a commodity trading manager, exempt market dealer, portfolio manager and investment fund manager. AIC is also registered as an exempt market dealer and portfolio manager in each province of Canada and may also be registered as an investment fund manager in certain other applicable provinces.

Aviva Investors Americas LLC is a federally registered investment advisor with the U.S. Securities and Exchange Commission. Aviva Investors Americas is also a commodity trading advisor (“CTA”) registered with the Commodity Futures Trading Commission (“CFTC”) and is a member of the National Futures Association (“NFA”). AIA’s Form ADV Part 2A, which provides background information about the firm and its business practices, is available upon written request to: Compliance Department, 225 West Wacker Drive, Suite 2250, Chicago, IL 60606.