25 May 2021

18 May 2021 | Richard Colwell, Head of UK Equities

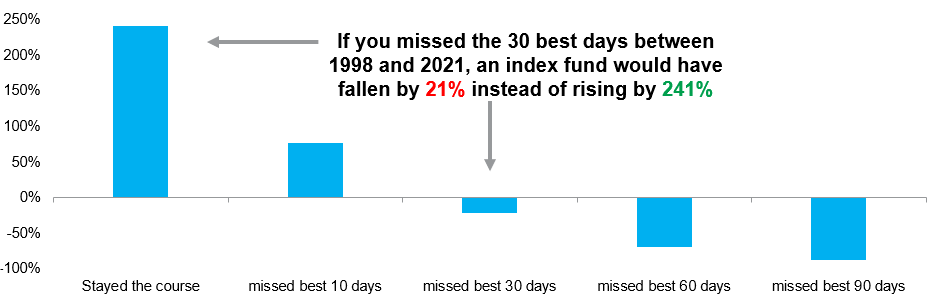

Figure 1: The fear of missing out – FTSE all share total cumulative return (1998-2021)

Source: Columbia Threadneedle Investments, Liberum, as at 22 March 2021

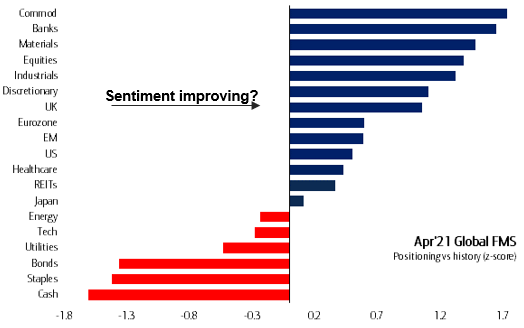

Figure 2: Global asset allocators had been reluctant to redress UK equities underweight

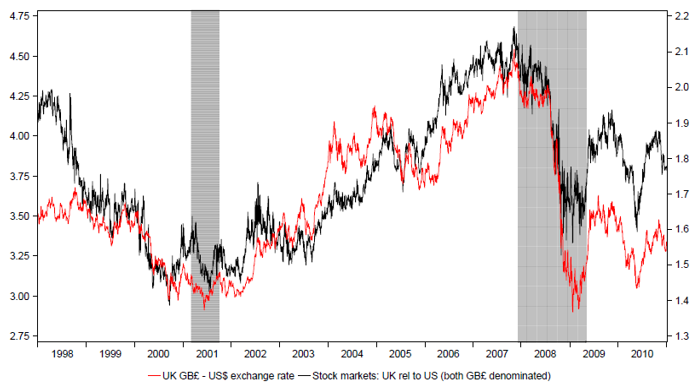

Figure 3: UK stock markets relative to US (shown with GB£-US$ spot rate)

The (portfolio) manager: Richard Colwell struts his stuff by the Charlton Athletic dugout

1 Bloomberg, 2020

2 Mention of specific stocks should not be taken as a recommendation

3 https://news.sky.com/story/morrisons-sees-sales-boost-from-coronavirus-lockdown-11986845 12 May 2020

4 Bloomberg, January 2021

5 Bloomberg, April 2021

6 Longview, December 2020

7 FT.com, Super League would break football’s essential promise, 19 April 2021

Important information

The research and analysis included on this website has been produced by Columbia Threadneedle Investments for its own investment management activities, may have been acted upon prior to publication and is made available here incidentally. Any opinions expressed are made as at the date of publication but are subject to change without notice and should not be seen as investment advice. Information obtained from external sources is believed to be reliable but its accuracy or completeness cannot be guaranteed.