14 Jan 2022

The medium-term outlook for the current cycle remains healthy and supportive for equity markets. However, there are several near-term risks. Short-term growth momentum is slowing, key central banks are moving towards faster policy normalisation, and there is another wave of Covid-19 forming.

Offsetting these concerns are robust household balance sheets, tentative signs of policy easing in China, peaking supply chain bottlenecks, and strong corporate earnings. Higher volatility has led to improved positioning metrics, and our risk-aversion models are also recovering. However, we remain neutral in our positioning on equities, with an increasingly positive bias on the short-term outlook.

Within equity regions, we remain positive on emerging markets. We are increasingly selective in developed markets, as we reduce the UK from neutral to underweight. Consumers in the UK are under pressure from slowing growth, rising activity restrictions related to the deteriorating Covid picture, and higher inflation and cost of living combined with tax rises and withdrawal of pandemic support.

As the Fed has announced tapering, we maintain our underweight US duration. Conversely, the market has largely priced out the BoE hawkishness, so we close out the gilt overweight after strong performance. ECB policy is expected to diverge further from the Fed's, and we upgrade bunds to neutral from underweight. In credit, we maintain our preference for higher yielding credit markets with default risk expected to remain low.

In FX we maintain our long US dollar position, which can benefit from a tighter Fed and looser fiscal in the US, and offers a hedge for the portfolio if central bank liquidity withdrawal becomes an issue.

![]()

The emergence of the Omicron variant has the potential to be a game-changer for the near-term macro and market outlook – and should be treated as such. The speed of the policy reaction has been notable. Policymakers, having learned from mistakes related to Delta, seem determined to act pre-emptively this time around. To gauge the potential economic fallout, we are tracking key viral variables including symptom severity, vaccine resistance and transmissibility compared to other variants. Recent news flow about the severity of disease after contracting Omicron has been encouraging, though the speed of transmission is now clearly shown to be orders of magnitude higher than previous variants. Restrictions are being stepped-up in a number of countries across the globe.

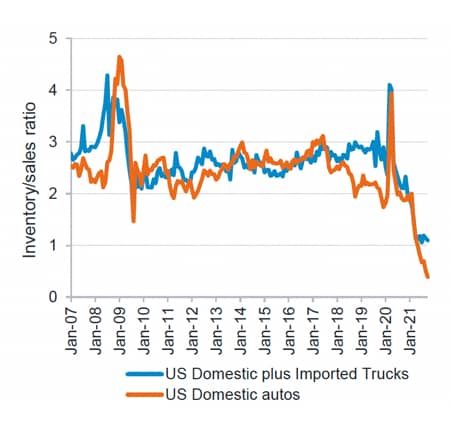

Were it not for Omicron, there were some indications that re-reflation could have taken hold as the dominant narrative in early 2022. Over the last several weeks, there has been evidence of the US labour market repairing, resilient corporate earnings supported by developed market demand and a helpful pivot towards easing in China. Indeed, over the longer-term, the two legs of potential re-reflation appear intact, specifically a high level of excess savings and depressed inventories presaging a restocking cycle.

Chart 1: Inventory restocking should drive re-reflation in 2022

Source: Haver, Fidelity International, December 2021.

Still, we recognize that Omicron has increased stagflationary risks for H1 2022, due to a potential combination of growth slowdown and inflationary effects as global supply chains are once more disrupted. This will exacerbate the Catch-22 dilemma in 2022 for central bankers, who find themselves caught between defending credibility on inflation while preserving the trajectory of the recovery and maintaining real negative rates.

With facts on the ground changing month-to-month, policymakers have been forced to pivot rapidly to address the increasing drumbeat of very high inflation. Despite Omicron uncertainty, the Federal Reserve doubled the pace of asset purchase tapering at its December FOMC meeting and opened the door to three rate hikes in 2022, while the BoE ended Covid emergency accommodation with a 15bp hike. As expected, the ECB remained comparatively dovish, guiding away from rate hikes in 2022 and maintaining flexibility to adjust its QE programmes to counter any unexpected negative future shocks.

We believe that the Fed will need to continue to walk a fine line in 2022, because of its implicit policy objective of maintaining negative real rates to support financial conditions and maintain debt sustainability.

Central banks in emerging markets will also face difficult choices given the pressure from the China slowdown, the effect of domestic tightening throughout 2021, and the global liquidity withdrawal by the DM central banks. Emerging markets will remain vulnerable to external shocks including variants and energy and food inflation. On the positive side, however, China appears committed to ensuring a soft landing related to the government’s reform of its “three mountains” of property, education and healthcare. As a result, the PBOC is likely to continue with as much accommodation as the government requires, which should mitigate tail risks of severely negative macro outcomes.

2022 is likely to be yet another year of unprecedented firsts - and potentially the end of a decades-long bull market in DM government bonds. We expect high volatility both in business and policy cycles, with inflation coming off its peak but settling at a steady state significantly above pre-Covid levels. Decarbonization and net zero targets will be a critical theme again in 2022 and far beyond, as private capital continues to surge into low carbon technologies and away from high-emissions sectors.

Geopolitics will continue to impact supply chains and resource availability, with Russian gas supply into Europe and heightened tensions at the Russia-Ukraine border being key focal points. The US-China economic rivalry will persist as a fundamental driver of the macroeconomy and markets. Developments in trade and investment relations next year may have material implications for corporate investment, the capital markets and more.

With multi-year fiscal programmes underway in the EU and US and a growing level of gridlock in the latter, attention is likely to turn to economic regulation. We expect the White House to focus on big tech, climate change and minimum wage (domestically) and to pursue advancement of its minimum tax agreement proposal (internationally). Anticipation of gridlock in the US Congress after November 2022 could presage an acceleration of policy activity. Across the world, China’s regulatory programme to support “common prosperity” will also continue to have implications far beyond its borders. Once again, 2022 will be new territory for investors, giving truth to the adage “May you live in interesting times.”

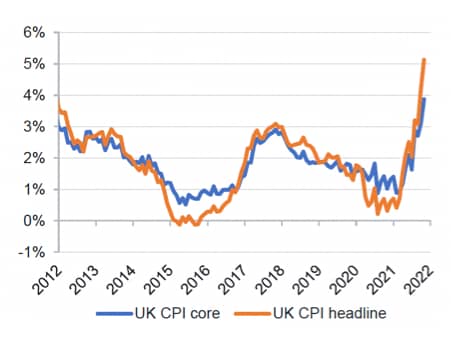

Chart 2: BoE acts to protect credibility over inflation

Source: Refinitiv, Fidelity International, December 2021.

Fidelity’s Global Macro & SAA team contributes to Fidelity Solutions & Multi Asset’s tactical asset allocation process by providing key macro inputs, working alongside the investment team to understand and respond to the macroeconomic drivers of markets.

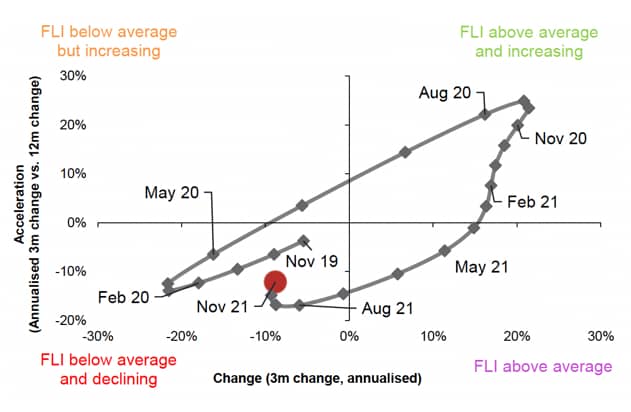

The FLI Cycle Tracker remains in the ‘bottom-left’ quadrant (below average and declining) but is showing some minor support. The 3-month FLI change could be stabilising at a double-digit rate. Yet the latest Omicron variant and its rapid transmissibility could put another dent in the recovery in early 2022. The FLI quantitative bet remains negative, pointing to a risk-off view, combined with a long duration position, but continues to move away from its highest conviction reading in September.

FLI Cycle Tracker

Source: Fidelity International, December 2021.

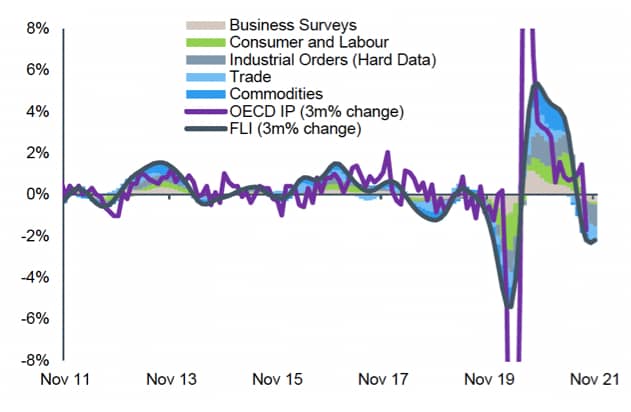

FLI: 3-month % change versus OECD IP

Source: Fidelity International. December 2021.

Four out of the five sectors are in the bottom-left quadrant, with indicators declining and below average. Commodities stand out and have moved back in the bottom-right quadrant with indicators declining but above average. Australian forward orders have picked up and the direction of travel seems to be improving for the Baltic Dry Index as well. Early signs that China may be past the worst with regulations easing and more supportive monetary policy could support broad commodities from here.

The Consumer and Labour sector has stabilized in the bottom-left quadrant below average and declining. As Covid cases start to rise again, due to seasonality and the Omicron variant, consumer confidence has weakened across the board and especially in the US. Levels remain fairly good though, particularly in Germany.

The FLI is a proprietary quantitative tool, designed to anticipate the direction and momentum of global growth over the coming months, and - importantly for investors - identify its key drivers. In practice, it is designed to lead global industrial production and other global cyclical variables by around three months. Fidelity Solutions & Multi Asset uses this as a common and repeatable reference point through the tactical asset allocation process.

Download the PDF to read the full Insight

Global Asset Allocation Insights January (PDF)

Important information

This material is for Institutional Investors and Investment Professionals only, and should not be distributed to the general public or be relied upon by private investors.

This material is provided for information purposes only and is intended only for the person or entity to which it is sent. It must not be reproduced or circulated to any other party without prior permission of Fidelity.

This material does not constitute a distribution, an offer or solicitation to engage the investment management services of Fidelity, or an offer to buy or sell or the solicitation of any offer to buy or sell any securities in any jurisdiction or country where such distribution or offer is not authorised or would be contrary to local laws or regulations. Fidelity makes no representations that the contents are appropriate for use in all locations or that the transactions or services discussed are available or appropriate for sale or use in all jurisdictions or countries or by all investors or counterparties.

This communication is not directed at, and must not be acted on by persons inside the United States. All persons and entities accessing the information do so on their own initiative and are responsible for compliance with applicable local laws and regulations and should consult their professional advisers. This material may contain materials from third-parties which are supplied by companies that are not affiliated with any Fidelity entity (Third-Party Content). Fidelity has not been involved in the preparation, adoption or editing of such third-party materials and does not explicitly or implicitly endorse or approve such content. Fidelity International is not responsible for any errors or omissions relating to specific information provided by third parties.

Fidelity International refers to the group of companies which form the global investment management organization that provides products and services in designated jurisdictions outside of North America. Fidelity, Fidelity International, the Fidelity International logo and F symbol are trademarks of FIL Limited. Fidelity only offers information on products and services and does not provide investment advice based on individual circumstances, other than when specifically stipulated by an appropriately authorised firm, in a formal communication with the client.

Europe: Issued by FIL Pensions Management (authorised and regulated by the Financial Conduct Authority in UK), FIL

(Luxembourg) S.A. (authorised and supervised by the CSSF, Commission de Surveillance du Secteur Financier), FIL Gestion (authorised and supervised by the AMF (Autorité des Marchés Financiers) N°GP03-004, 21 Avenue Kléber, 75016 Paris) and FIL Investment Switzerland AG. .

In Hong Kong, this material is issued by FIL Investment Management (Hong Kong) Limited and it has not been reviewed by the Securities and Future Commission.

FIL Investment Management (Singapore) Limited (Co. Reg. No: 199006300E) is the legal representative of Fidelity

International in Singapore. This document / advertisement has not been reviewed by the Monetary Authority of Singapore.

In Taiwan, Independently operated by Fidelity Securities Investment Trust Co. (Taiwan) Limited 11F, No.68, Zhongxiao East Road, Section 5, Taipei 110, Taiwan, R.O.C. Customer Service Number: 0800-00-9911

In Korea, this material is issued by FIL Asset Management (Korea) Limited. This material has not been reviewed by the Financial Supervisory Service, and is intended for the general information of institutional and professional investors only to which it is sent.

Fidelity is authorised to manage or distribute private investment fund products on a private placement basis, or to provide investment advisory service to relevant securities and futures business institutions in the mainland China solely through its Wholly Foreign Owned Enterprise in China - FIL Investment Management (Shanghai) Company Limited.

Issued in Japan, this material is prepared by FIL Investments (Japan) Limited (hereafter called “FIJ”) based on reliable data, but FIJ is not held liable for its accuracy or completeness. Information in this material is good for the date and time of preparation, and is subject to change without prior notice depending on the market environments and other conditions. All rights concerning this material except quotations are held by FIJ, and should by no means be used or copied partially or wholly for any purpose without permission. This material aims at providing information for your reference only, but does not aim to recommend or solicit funds /securities.