14 Aug 2024

As we move further away from a decade of ultra-loose monetary policy, bonds are once again proving their attractive diversification benefits. Our UK fixed income portfolio managers reflect on the recent bout of market volatility and outline the benefits of duration in an environment where investors are increasingly sensitive to weak macro data.

Key points

We often discuss the role of bonds in a well-diversified portfolio, notably in offering a stable level of income, modest volatility and diversification away from equity markets. While the income benefit was modest (at best) during the period of ultra-easy monetary policy (2010-2021) it is back now with yield levels attractive once again.

Most investors would agree that it was a painful experience to get here, particularly during 2022 when high quality bond markets suffered severe drawdowns. This was a period when equity-bond correlations moved higher - and positive - with stocks and bonds selling off in tandem, prompting many investors to question whether bonds provide diversification benefits. The good news is, as inflation fades, bonds are proving their diversification-worth once again, with the latest bout of volatility in stock markets a timely reminder of that.

Cumulative returns over the last month

.png)

Past performance is not a reliable indicator of future results. Returns may increase or decrease as a result of currency fluctuations.

Source: Fidelity International, Bloomberg, 5 August 2024.

Equity market jitters

Poor data via the manufacturing ISM report on 1 August and the employment report (note the distortions from Hurricane Beryl) on 2 August together cast a shadow of doubt over the US economy. Up until then, the US economy had in the eyes of the market (and contrary to our views) been gliding to a perfect soft landing. This led to a sharp fall in stock markets while government bonds rallied. The Bank of Japan’s decision to hike rates during the same week, and news over the weekend of Berkshire Hathaway selling down its stake in Apple, triggered further selling, with the TOPIX experiencing its worst day since October 1987. Markets have since retraced some of these losses, but volatility remains elevated.

More duration = greater diversification

The good news for risk averse investors who wish to diversify their higher risk exposures is that high quality bonds have performed well during this period. Furthermore, bonds with more interest rate risk (longer duration) have outperformed bonds with less interest rate risk.

Longer dated bonds have outperformed: Total returns 1 July - 5 August 2024

.png)

.png)

Past performance is not a reliable indicator of future results. Returns may increase or decrease as a result of currency fluctuations.

Source: Fidelity International, Bloomberg, 5 August 2024.

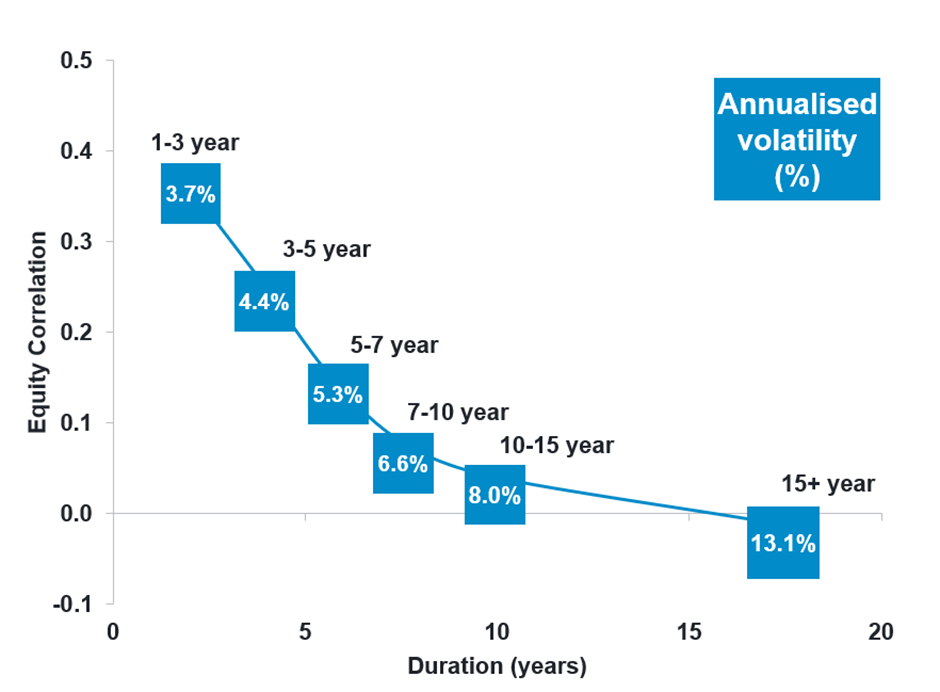

Higher duration levels and lower equity correlations are something that can be observed over the longer term as well. Looking at data from 2002 and simulating different duration levels by adding excess returns of the Sterling Corporate Index onto different UK Gilt Indices by maturity, we can see that greater duration levels are associated with lower equity correlations. However, there is no free lunch, one must be willing to shoulder the greater volatility that comes with taking more interest rate risk. As shown, the 1-3yr part of the curve is associated with an equity correlation of +0.4 and a long run annualised volatility rate of 3.7%, versus the 15+ year part of the curve at a 0.0 correlation but with volatility at over 13%.

Duration vs correlation to equities

Source: Fidelity International, Bloomberg, 4 February 2024. Simulates duration reduction by adding excess returns of Sterling Corporate Index (UR00) onto UK Gilt Indices (by maturity). BoA indices used. Data from 2002.

We expect equity-bond correlations to move negative once again

During severe risk-off periods, and in the absence of elevated inflation, interest rate risk can provide a powerful diversifier against equity markets. The 2022 episode was an exception to the norm with both equities and bonds selling off as inflation rose to elevated levels, prompting central banks to aggressively hike interest rates. With the inflation shock now behind us and with central banks globally moving to an easy policy stance, we expect equity bond correlations to fall during risk-off events - such as those seen in early August.

Stocks have rallied back since, but there are a few important takeaways from this period of heighted volatility; i) with inflation now at or around central bank target levels, high quality bonds are once again providing diversification away from stocks, ii) related to this, increasing duration lowers the equity-bond correlation, but is accompanied by increased volatility ;and iii) the market is sensitive to poor economic data, bad news is once again bad news. Against this backdrop, we maintain a long interest rate risk position across the portfolios.

Important information

This information is for investment professionals only and should not be relied upon by private investors. Past performance is not a reliable indicator of future returns. Investors should note that the views expressed may no longer be current and may have already been acted upon. Changes in currency exchange rates may affect the value of investments in overseas markets. Fidelity’s range of fixed income funds can use financial derivative instruments for investment purposes, which may expose it to a higher degree of risk and can cause investments to experience larger than average price fluctuations. The value of bonds is influenced by movements in interest rates and bond yields. If interest rates and so bond yields rise, bond prices tend to fall, and vice versa. The price of bonds with a longer lifetime until maturity is generally more sensitive to interest rate movements than those with a shorter lifetime to maturity. The risk of default is based on the issuers ability to make interest payments and to repay the loan at maturity. Default risk may therefore vary between government issuers as well as between different corporate issuers. Due to the greater possibility of default, an investment in a corporate bond is generally less secure than an investment in government bonds. Reference in this document to specific securities should not be interpreted as a recommendation to buy or sell these securities and is only included for illustration purposes.