24 Mar 2025

Mike Riddell, portfolio manager of Fidelity Strategic Bond Fund, provides an overview of the macroeconomic environment and outlines his views across the strategy’s main alpha sources. Against a backdrop of increased global market volatility, potentially signalling the end of the US exceptionalism trade, he outlines why the team has become less bullish on US Treasuries in the context of less attractive valuations.

Key points

Under the first Trump presidency, it took about three months for the similar ‘Trumponomics’ macro narrative to unwind. If anything, it’s been even faster under Trump 2.0. The unwinding of the US exceptionalism trade has propelled US Treasury prices higher as investors moved to reprice in some of the Fed rate cuts that had been priced out in Q4 2024. Whilst we still believe that US growth can continue to disappoint expectations over the remainder of the year, we have become less bullish on US Treasuries in the context of less attractive valuations.

We think the recent huge selloff in bunds, on the back of infrastructure spending plans and announcements of increased defence spending, look overdone. Market participants now appear too optimistic on the growth outlook for Europe, bearing in mind material infrastructure spending will take many years to be implemented, and are overlooking the negative growth impact risk of US tariffs on the Eurozone.

We continue to be concerned about the UK labour market. Despite recent improvements in UK data, the UK has zero productivity growth, and we expect wage growth to slow.

We continue to think a global stagflationary environment is a reasonable possibility, and the market still doesn’t appear to be pricing in any real risk of ‘stag’. We maintain our long duration positioning at a fund level.

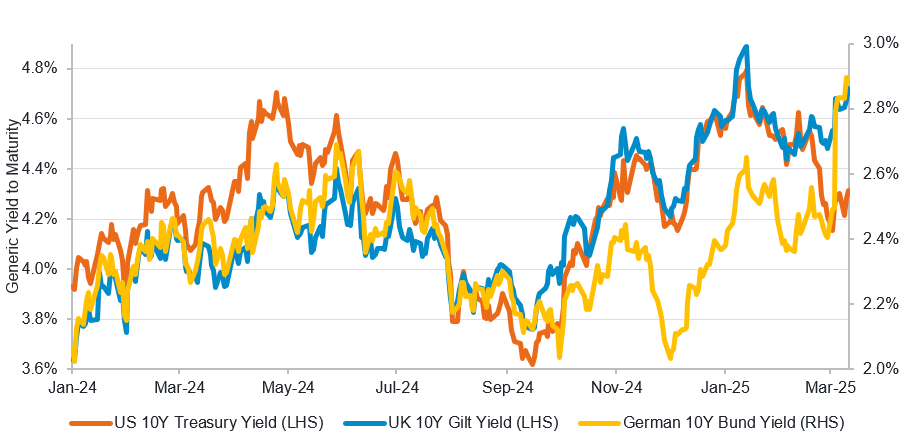

Government bonds remain extremely volatile on geopolitical uncertainty

Source: Bloomberg, 12 March 2025. Data based on GT10 Govt, GUKG10 Index and GDBR10 Index.

Below we outline our views on four sources of alpha within the strategy: rates inflation, currencies and credit.

Rates

We retain a moderate long overall duration in the funds, with overweight positioning in the UK and Europe versus other global rates markets.

Following a substantial rally in US Treasuries, we have taken profits on our long US duration position. With more Fed rate cuts priced in, we are less bullish on US Treasuries in the context of less attractive valuations and are now neutral US duration. We have recently increased our long UK duration position. Whilst recent data prints have improved, we think that the underlying UK labour market is weak with zero productivity growth.

Following the recent huge bund selloff, we moved shorter Canada duration and trimmed US duration in order to enter a long German duration position, where relative valuations to switch are the cheapest since the Eurozone debt crisis. Considering the European defence sector is already close to full capacity, we aren’t convinced that the defence spending will be as big as the market expects, and in any case the spending will realistically take many years to implement. We remain generally underweight Euro duration outside of bunds.

We have added to our long Brazil duration position and have entered into a long Colombia duration position. Emerging market (EM) local rates have lagged the US Treasury rally, as well as lagging the BRL rally vs USD which is normally highly correlated. Brazil real yields have also been flagged as historically cheap by our EM cross-market rates model.

We maintain our long Norway vs short Sweden RV trade as Norway’s implied rates are high compared to Sweden’s.

Inflation

We remain moderately long inflation at a fund level, as we think there is the potential for inflation surprises to the upside, as we have seen in Norway and Sweden.

We maintain our small long Euro breakeven inflation position in the funds, as we still believe the market is not pricing in that much inflation in Europe, which may be stickier than the market expects.

Currencies

We have entered into most of our long EM rates positions unhedged, which gives us currency exposure. We are long Indonesian Rupiahs, Columbian Peso, Brazilian Peal and Mexican Peso versus the US Dollar/Pound Sterling.

Meanwhile the US Dollar looks expensive versus EM currencies, and we continue to believe that a weaker dollar would support EM currencies.

Credit

We have maintained our underweight credit positions and are currently running a 0.8 credit beta.

Credit spreads have been closely correlated to equities since June 2024, and spreads are very tight compared to historical averages. We see more downside risk than upside potential from here and remain cautious on credit.

Important information

This information is for investment professionals only and should not be relied upon by private investors. Past performance is not a reliable indicator of future returns. Investors should note that the views expressed may no longer be current and may have already been acted upon. Changes in currency exchange rates may affect the value of investments in overseas markets. Fidelity’s range of fixed income funds can use financial derivative instruments for investment purposes, which may expose them to a higher degree of risk and can cause investments to experience larger than average price fluctuations. The value of bonds is influenced by movements in interest rates and bond yields. If interest rates and so bond yields rise, bond prices tend to fall, and vice versa. The price of bonds with a longer lifetime until maturity is generally more sensitive to interest rate movements than those with a shorter lifetime to maturity. The risk of default is based on the issuers ability to make interest payments and to repay the loan at maturity. Default risk may therefore vary between government issuers as well as between different corporate issuers. Due to the greater possibility of default, an investment in a corporate bond is generally less secure than an investment in government bonds. Reference in this document to specific securities should not be interpreted as a recommendation to buy or sell these securities and is only included for illustration purposes.