28 Apr 2023

Benedict Buckley, CFA, Portfolio Analyst

ClearBridge Investments: Actions to mitigate and adapt to climate change will disrupt many sectors, creating both winners and losers.

Decarbonization is increasingly sparking debate about its urgency and possibility, as governments and corporations continue to commit to net zero. It is driving innovation in many sectors, with industries aiming to lower carbon emissions while still enabling the global economy to thrive.

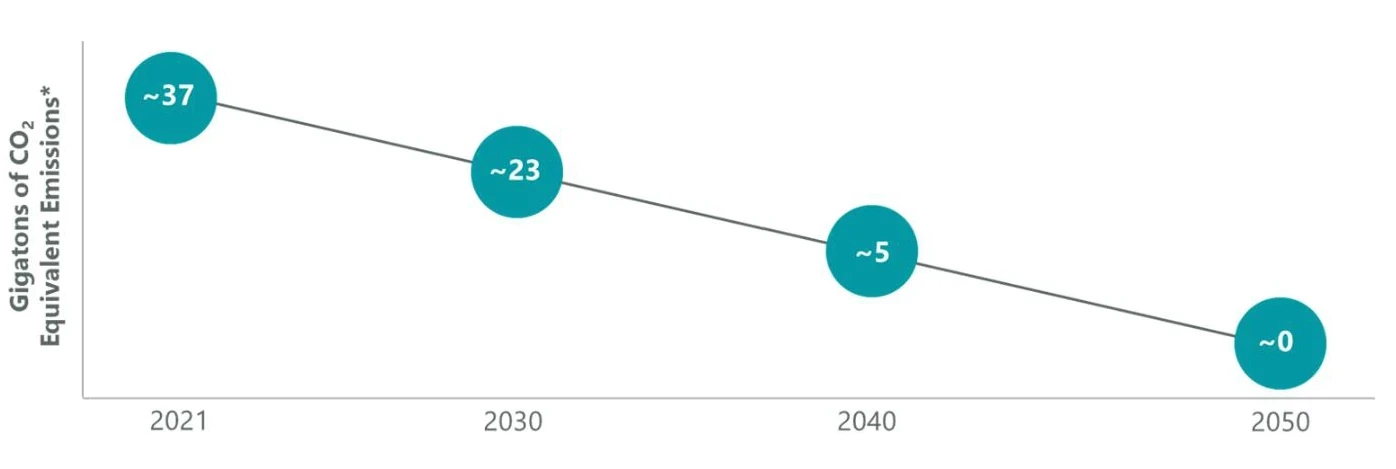

Decarbonization, simply put, means reducing the global economy’s annual carbon emissions to net zero. Doing this by 2050 would enable us to meet the goal of limiting global temperature rise to 1.5° Celsius and help us avoid the worst effects of global warming (Exhibit 1).

Exhibit 1: Pathway to Net Zero by 2050 is Narrow but Achievable

Source: *Adapted from International Energy Agency (2022), World Energy Outlook 2022.

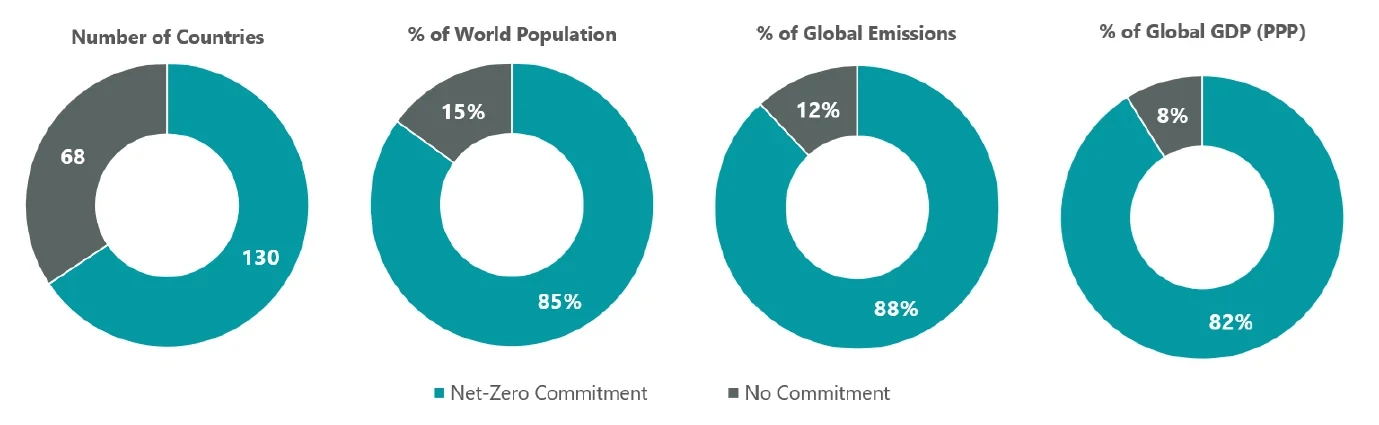

A significant portion of the global economy has committed to reaching net zero: roughly 92% of global GDP, accounting for 88% of global emissions and 85% of the world’s population has made net-zero commitments (Exhibit 2). Most countries have set 2050 as a date to reach net-zero carbon emissions, while some have earlier target dates (Germany and Sweden are targeting 2045) or later (China’s goal is 2060, and India’s is 2070).

Exhibit 2: Portion of World Covered by Net-Zero Commitments

As of March 2023. Source: Net Zero Tracker.

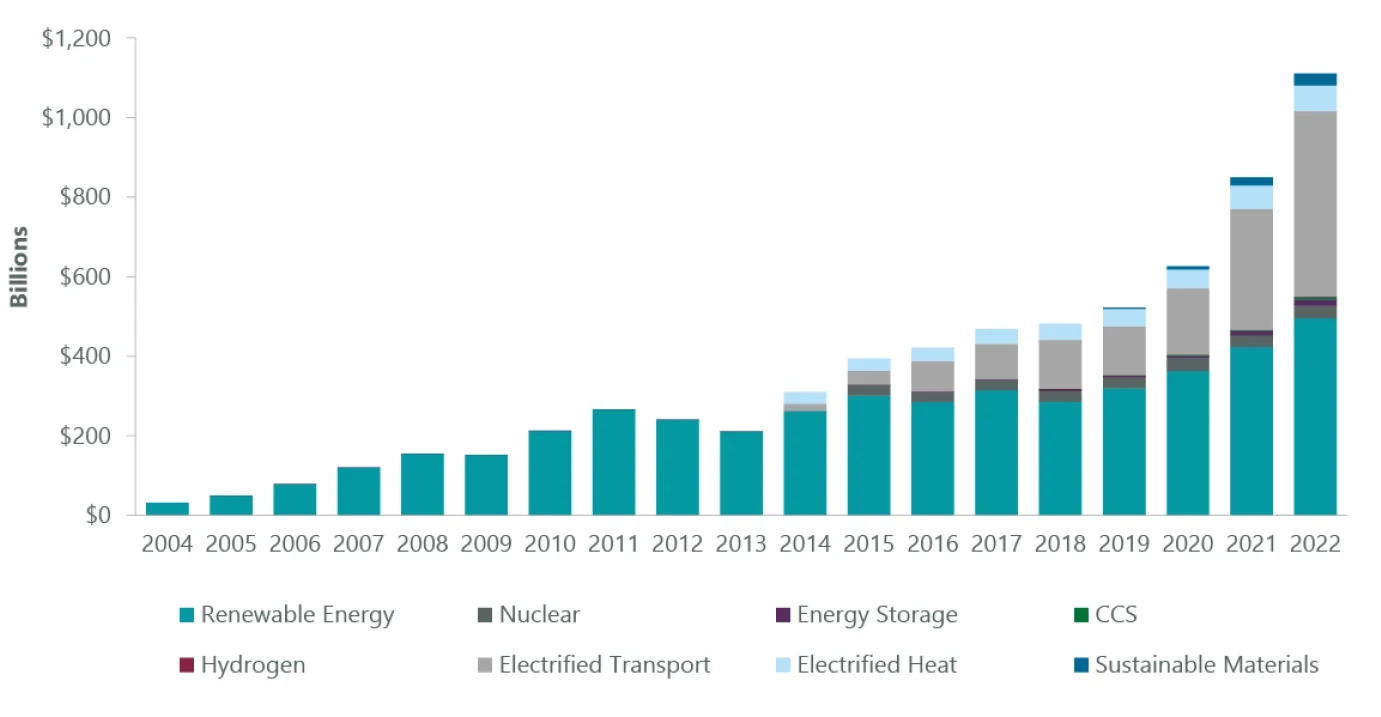

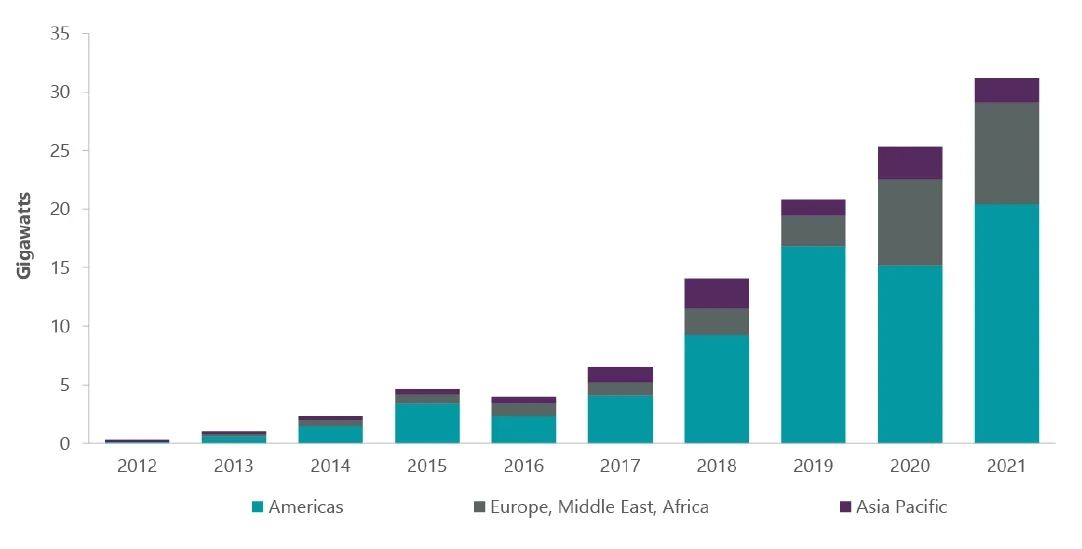

The wave of government commitments to net zero is a key pillar of the investment case for decarbonization. The other key pillar is technological change, which continues to drive down the cost of decarbonization solutions. Decarbonization is a key secular theme that will have long-term implications on the global economy. It will drive an immense amount of investment: between $3 trillion and $4 trillion per year is required globally to meet the goals of the Paris Climate Agreement. According to BloombergNEF (BNEF), ~$1.1 trillion was invested in clean energy in 2022 (Exhibit 3). While this was an impressive 31% increase versus 2021, these investment levels still need to triple to get on track for net zero, so we expect the level of investment to ramp up over time. Importantly, this investment will span multiple sectors.

There is a clear opportunity for businesses — companies that can solve decarbonization challenges will get rewarded, as there are large addressable markets for companies innovating and finding new ways to perform almost any economic activity in a way that is lower carbon. This includes scaling up existing technologies, as well as commercializing new technologies; there is roughly equal need for both, according to analysis by Bank of America.

Exhibit 3: Global Energy Transition Investment by Sector

Note: Start years differ by sector, but all sectors are present from 2019 onward. As of Jan. 2023. Source: BNEF, “Energy Transition Investment Trends 2023.”

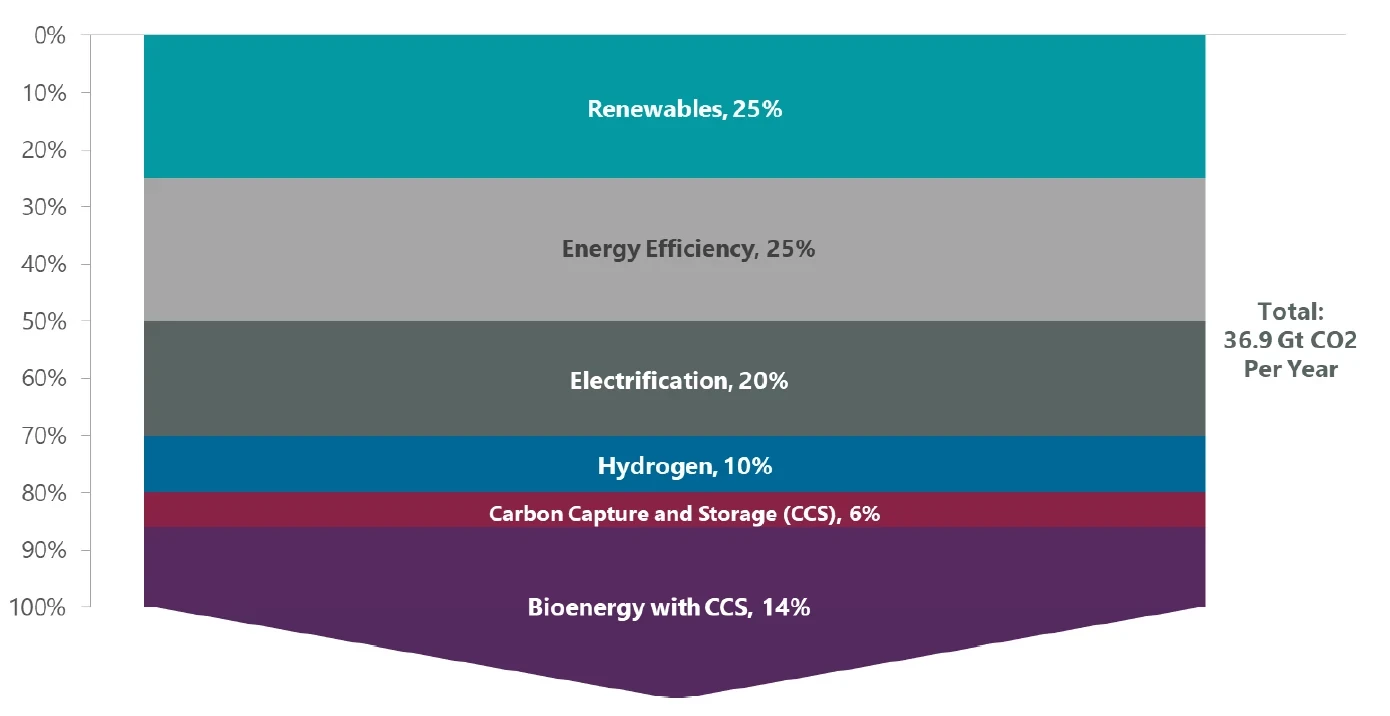

Broadly, there are six components to the energy transition (Exhibit 4). The first major decarbonization transition is occurring in the power sector, where wind and solar are replacing coal and gas. While there are policies encouraging this transition in some jurisdictions, it is being driven primarily by economics as technology advancements are lowering the levelized cost of electricity from wind and solar (Exhibit 5).

Exhibit 4: Components of Energy Transition

Source: International Renewable Energy Agency.

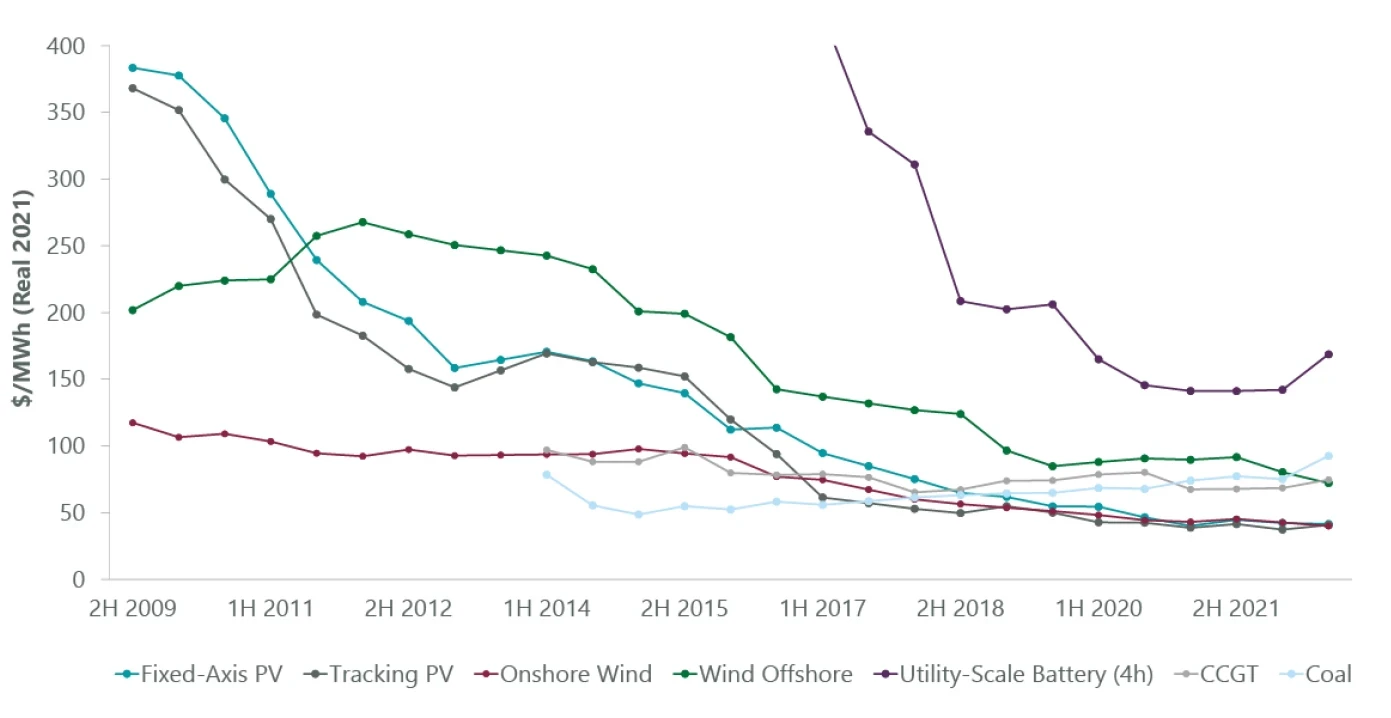

Exhibit 5: Wind and Solar Now Cheaper than Coal

As of March 2023. Source: BNEF 2H 2022 Levelized Cost of Electricity.

Even with temporary cost increases for renewables in the form of higher interest rates, the gap to fossil fuel power generation continues to widen due to fuel and carbon prices rising even faster. New-build onshore wind and solar projects are now around 50% lower than BNEF’s global benchmarks for new coal- and gas-fired power. We have seen exponential cost reductions in wind (~50%) and solar (~90%) in the past decade. Solar and wind are now the cheapest forms of energy in countries with two-thirds of the global population and 90% of world electricity generation.

Accordingly, many industries offer ways to invest in decarbonization, including: mobility; renewable energy and storage; building efficiency; industrial efficiency and products; food and agriculture; technology and software; and materials. Across this wide range of industries, there are many different business models at different stages of maturity, suggesting the need for being selective. Key decarbonization industries include:

While there are clear opportunities driven by decarbonization, there are also challenges to consider. Companies able to address and help overcome these challenges may see attractive market opportunities.

Grid interconnection and project permitting: Hooking up a renewable energy project to the grid can present a challenge to developing renewable energy. Currently, there are 1,900 renewable power projects in the U.S. awaiting interconnection5 while the Federal Energy Regulatory Commission (FERC) looks to reform interconnection procedures to reduce the backlog. Meanwhile, permitting remains a problem for renewable projects and for the additional transmission lines needed to move the power from its source to large demand centers like cities — both can face fierce local opposition from residents.

Raw material availability: Clean energy technologies such as solar panels, wind turbines, batteries and electric motors require more critical minerals than the conventional technologies they are replacing. This means the transition to clean energy will lead to significantly higher demand for minerals such as copper, lithium, nickel, cobalt and rare earth elements. In fact, reaching net zero globally by 2050 would require up to 6x more mineral inputs in 2040 than today.6 This creates significant challenges as some of these materials have limited geographic availability and entail meaningful environmental and social risks to produce. Securing enough critical minerals to enable decarbonization is a key hurdle to achieving net zero.

Climate justice: There are two elements to climate justice. Firstly, countries are experiencing differing levels of disruption from the physical impacts of climate change — such as sea level rise, or increased weather events like floods, wildfires and droughts. The cost of responding to extreme weather events can be a significantly larger burden for countries with smaller economies that are less able to afford the investments.

While climate change is already exacerbating hardships for vulnerable people in countries all around the world, the transition to a net-zero economy won’t be politically viable (or morally acceptable) if the transition exacerbates existing inequalities, for example by increasing energy costs at unacceptable rates. This is sometimes referred to as the need for a “just transition.” One-third of U.S. households already face some form of energy poverty, whether it is unaffordable energy bills, forgoing basic necessities like food and medicine, or the inability to keep the home at a healthy temperature.

There are also impacts to certain communities from the winding down of carbon-intensive industries such as coal mining. These communities will likely need to be supported through the transition. For example, in the U.S., the Inflation Reduction Act includes extra incentives for building clean energy projects or manufacturing plants in such communities — with the hope that these communities can receive some of the economic benefits from deployment of low-carbon technologies.

Deglobalization: Several related geopolitical developments are causing globalization to go into reverse. We are seeing a rise in trade tariffs and national industrial policies that prioritize domestic production for key industries like semiconductors and energy. For decarbonization to occur at the pace required to reach net zero by the middle of this century, however, we need more international cooperation, not less. In support of this, the International Energy Agency and the International Renewable Energy Agency (IRENA) call for common standards, technology sharing and the removal of trade barriers.

In addition to seeking out winners in industries most affected by decarbonization, active managers can encourage portfolio companies to make specific changes that lead to real-world emissions reductions.

While most companies don’t sell a product that directly reduces emissions, all companies can play a role in addressing climate change by changing the way they operate. Companies are significant users of power, and their buying decisions make a difference (Exhibit 6).

Exhibit 6: Global Corporate Renewable Power Purchase Agreements

Source: Science-based Targets Initiative.

Corporations have become a key demand driver for renewable power. Renewable power purchase agreements (PPAs) provide companies with both long-term price visibility and help achieve emissions reduction goals. Effective active management can include engaging with company management to share and promote best practices as well as proxy voting to encourage more ambitious climate action where relevant.

A broad mix of regulatory policy, strategic decisions by companies, technological innovation and investor initiatives is supporting the investment case for decarbonization, driving change in several industries. ClearBridge has been active in furthering these positive trends and is also well positioned to benefit from them, investing in companies enabling the transition and engaging with companies to help them thrive and create value over the long term.

Endnotes

WHAT ARE THE RISKS?

Past performance is no guarantee of future results. Please note that an investor cannot invest directly in an index. Unmanaged index returns do not reflect any fees, expenses or sales charges.

Equity securities are subject to price fluctuation and possible loss of principal. Fixed-income securities involve interest rate, credit, inflation and reinvestment risks; and possible loss of principal. As interest rates rise, the value of fixed income securities falls. International investments are subject to special risks including currency fluctuations, social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets. Commodities and currencies contain heightened risk that include market, political, regulatory, and natural conditions and may not be suitable for all investors.

U.S. Treasuries are direct debt obligations issued and backed by the “full faith and credit” of the U.S. government. The U.S. government guarantees the principal and interest payments on U.S. Treasuries when the securities are held to maturity. Unlike U.S. Treasuries, debt securities issued by the federal agencies and instrumentalities and related investments may or may not be backed by the full faith and credit of the U.S. government. Even when the U.S. government guarantees principal and interest payments on securities, this guarantee does not apply to losses resulting from declines in the market value of these securities.

Any companies and/or case studies referenced herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. All investments involve risks, including possible loss of principal.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued by Franklin Templeton Investment Management Limited (FTIML). Registered office: Cannon Place, 78 Cannon Street, London EC4N 6HL. FTIML is authorised and regulated by the Financial Conduct Authority.

Investments entail risks, the value of investments can go down as well as up and investors should be aware they might not get back the full value invested.