01 Apr 2022

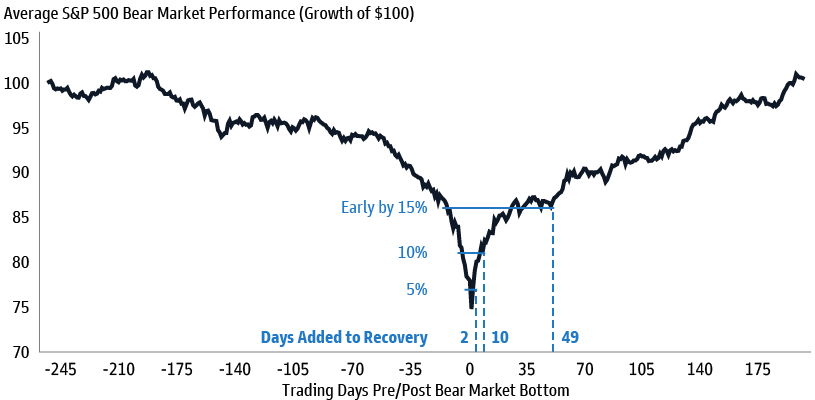

Chart of the Week: Cost of Being Early

Source: Goldman Sachs Asset Management.

MARKET SUMMARY

GLOBAL EQUITIES: US equities closed 1.81% higher this past week, as a strong jobless claims report and robust performance of semiconductor stocks outweighed oil price concerns. Meanwhile, European equities saw more tumultuous trading on the back of ongoing geopolitical tensions, an elevated UK CPI print, and the UK Spring Statement, which notably included a long-term tax reduction for workers and plans for an immediate fuel tax cut. The STOXX 600 and FTSE 100 finally ended the week at -0.15% and 1.16%, respectively.

COMMODITIES: Oil prices jumped last week as supply concerns due to Caspian pipeline disruptions were offset by division among EU leaders on plans to boycott Russian oil. WTI and Brent crude ended the week up at $113.90 and $120.65 per barrel, respectively.

FIXED INCOME: Yields moved higher in the US as jobless claims ticked lower, signaling a strong labor market that may continue to contribute to wage inflation. Last week the Fed also indicated that they would consider more aggressive rate hikes if needed, leading 2-Year and 10-Year Treasury yields to rise to 2.30% and 2.49%, respectively. European sovereign yields followed suit, with the 10-Year German Bund and UK Gilt yields also ending higher at 0.59% and 1.70%, respectively.

FX: The US dollar strengthened 0.54% against a basket of currencies as Fed officials signaled a path for potentially more aggressive rate hikes from the central bank in May. Meanwhile, the euro and pound sterling fell to $1.0987 and $1.3183, respectively, against the safe-haven US dollar as the US announced additional sanctions on Russia amidst the Russia-Ukraine conflict.

ECONOMIC SUMMARY

MANUFACTURING: US manufacturing PMI rose to an above-consensus 58.5 in March on the back of less stringent COVID-19 restrictions and a relative easing of supply chain constraints. In Europe, Euro area flash PMI fell in March to a higher-than-expected 54.5, reflecting a still strong private sector, although companies expect the war in Ukraine to weigh on European growth.

LABOR: US initial jobless claims printed at a 50-year low of 187k for the week ending March 19, below consensus expectations and down from 214k the week prior. The decline in claims reflects US labor market strength as workers rejoin the labor force and layoffs remain limited.

INFLATION: In the UK, headline CPI continued to rise in February to 6.2% year-over-year, the highest level recorded since the measure was introduced in 1997. The strength remained broad-based across all measures of underlying inflation, and underlying wage growth remained higher than the historical average.

SENTIMENT: Germany’s Ifo Business Climate index fell to 90.8, the lowest reading since January 2021, as higher energy prices and RussiaUkraine uncertainty dampened sentiment.

DOWNLOAD MARKET MONITOR

Access the full PDF to use with your clients

DOWNLOAD