18 Feb 2022

After years of underinvestment, the world is in the early stages of a potential global gas crisis. But with ambitious global climate targets largely incompatible with natural gas demand, uncertainty abounds.

The finger of blame for soaring natural-gas prices has been pointed in multiple directions: the weather, the pandemic, general gas production, a slowdown in shallow drilling, OPEC, geopolitical stresses, and so the list goes on. But the true source of this looming crisis is long-term underinvestment in a globally diversified, stable long-cycle supply base.

As a result, inflation and a real income squeeze are going to be felt by the world's poorest, particularly in Europe and Asia.

But how does the need to ramp up investment tally with the world’s climate ambitions?

Such uncertainty is likely to keep domestic investment down, particularly in Europe, which in time raises the chance of prolonged shortages globally. The US gas market may see this policy impact fall through to some significant long-term pricing support, as we see a global relinking of energy markets.

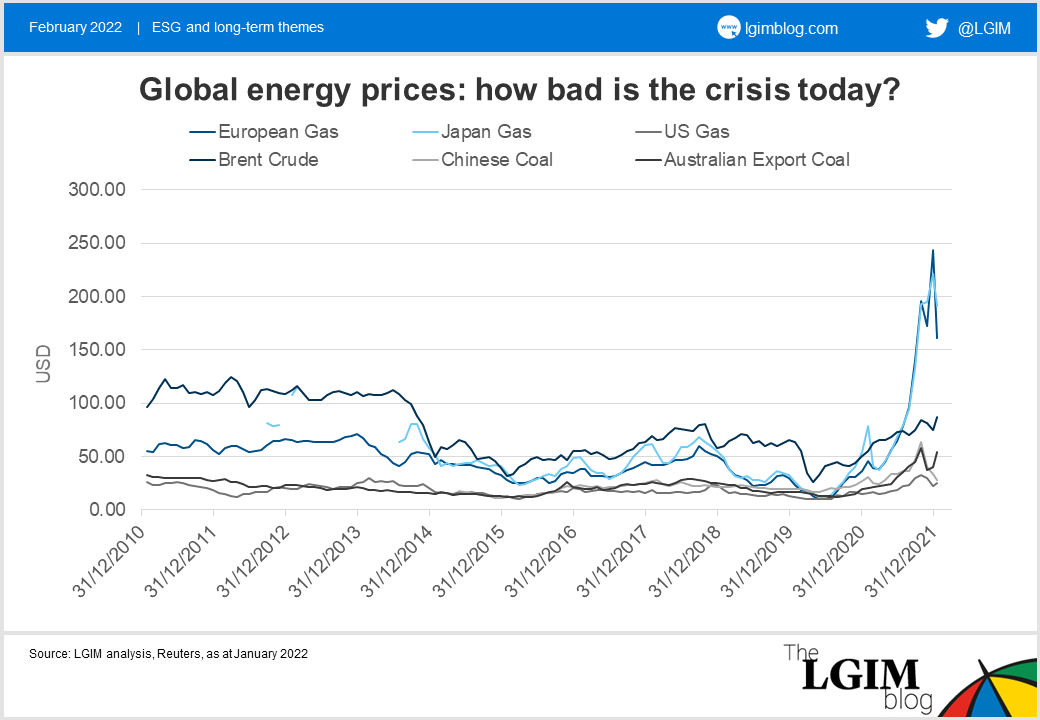

The gravitational pull of energy price parity is starting to be felt a bit more strongly – you can multiply the gas price by six to get to an equivalent price for a barrel of oil. So, with US gas prices at US$4, that's about the equivalent of US$24 for a barrel of oil, which is very cheap.

Both Europe and Asia see gas prices well north of US$150 a barrel in oil-equivalent terms today. Prices in Europe have spiked as high as US$250 a barrel on a one-month forward basis and over US$300 a barrel on a spot basis. That's an enormous price shock. It's being felt by industry first but is increasingly starting to feed through to consumers.

Much of the crisis in Europe is our own fault. The region has underinvested for a long time and demonised domestic gas supply, while doing little to address demand. That has only heightened its dependence on foreign gas supply. We expect that dependence to continue to grow, and quite rapidly, to at least 2030.

This is among the greatest price shocks that we've seen since the industrial period started and we don't think it's going to get much better. There’s a reasonable chance that we continue to see European gas shortages for some time, with a similar picture in Asia.

As a result, Europe and Asian gas markets are competing to secure cargoes, which means that prices are linking, and the two markets are competing in spot liquefied natural gas (LNG) markets. We continue to see US markets trade at this huge discount largely because there isn't enough liquefaction capacity to link the markets together effectively.

But over the longer term, we expect the US - in a policy-neutral world - to continue to expand its liquefaction capacity. That is going to increase the linkage, largely broken by the US shale revolution of the early 2000s, between domestic gas prices in the US and international gas pricing.

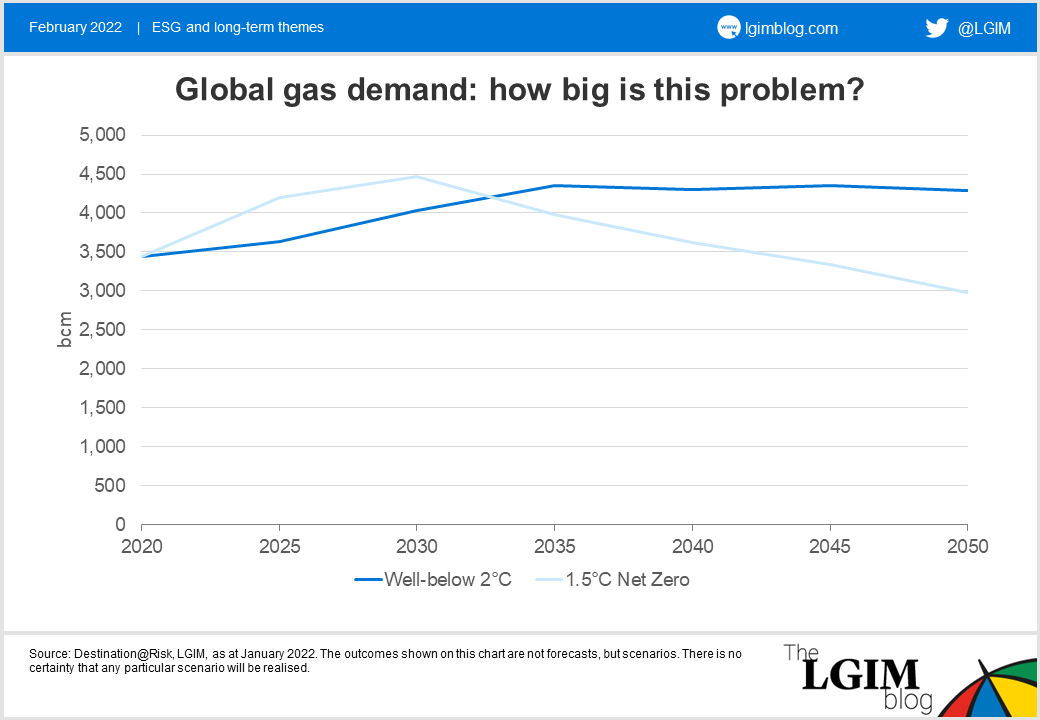

Our modelling suggests that ‘going for gas’ is an effective way of targeting a below 2°C outcome. However, it's not a plausible route to achieving a net-zero 1.5°C outcome. And if global aspirations remain to reach for the increasingly challenging target of net zero, the world is going to have to move away from natural gas.

As shown in the chart below, a 1.5°C climate outcome leaves very little room on a gross basis for natural gas. The chart shows two of the scenarios that we currently run in our Destination@Risk model. The lighter line is our net-zero 1.5°C scenario – there is a big gulf that opens up post 2030 in demand for natural gas, which is a function of the carbon budget.

As long as policymakers aspire to a net-zero climate outcome, there is little room for natural gas to continue to grow; it must shrink in the 2030s. But for now, supply-side and demand-side indicators simply do not paint the same picture. Uncertainty abounds.

Disclaimer: Views in this blog do not promote, and are not directly connected to any Legal & General Investment Management (LGIM) product or service. Views are from a range of LGIM investment professionals and do not necessarily reflect the views of LGIM. For investment professionals only.