04 May 2022

First-quarter earnings for 2022 have so far not delivered many upsets, even if the post-pandemic lustre is fading. Looking to next year, however, the red-hot US labour market could threaten earnings – making it all the more important to turn to a broad set of data points to build a picture of what to expect.

After a tough 2020, 2021 saw US corporate profits soar 25% – their largest gain in a single year since 1976.1

However, as we move on from the near euphoria of the post-pandemic re-opening, it is the very intensity of this growth and attendant overheating in the US labour market that could pose problems for earnings into 2023.

The trajectory of the American economy is difficult to forecast with any confidence. However, it is possible to start building a credible picture when we compare models and datasets where there is not a consensus – the gaps between them could hold useful insights for savvy investors.

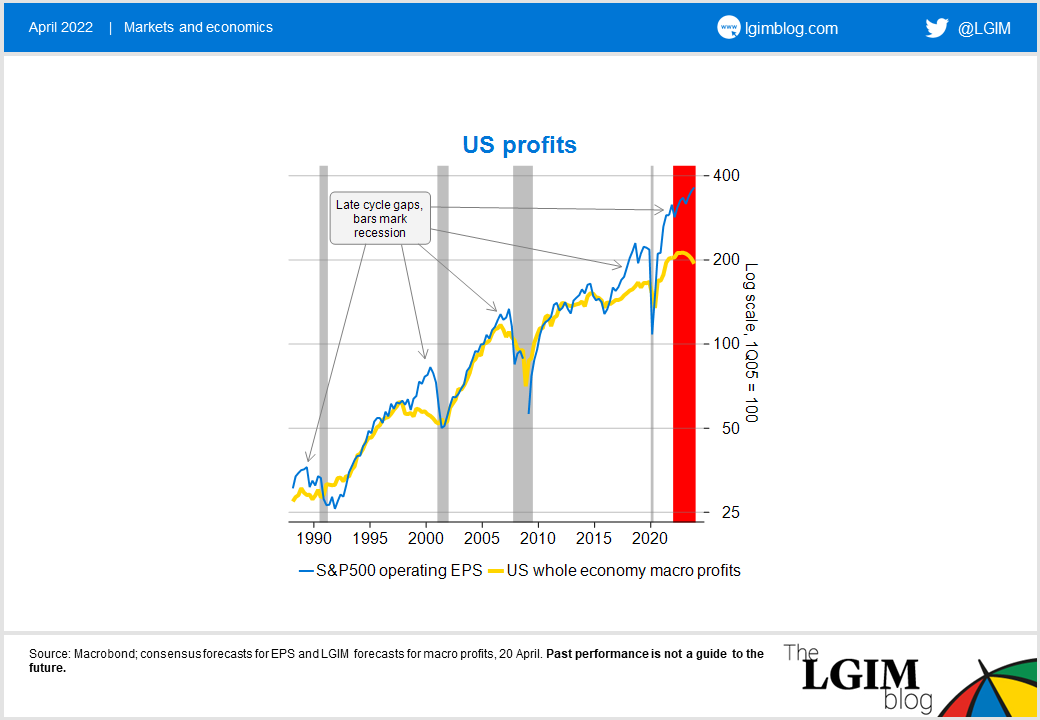

For example, we can gain different and complementary understandings on the state of US earnings if we focus on either the S&P 500 or the less widely reported US NIPA (National Income and Product Accounts).

These information sources diverge in subtle but significant ways: S&P 500 earnings are weighted toward the goods sector and their accounting treatment means they can tick upward late in the business cycle, whereas the NIPA data can lag reported earnings and are prone to revision.

We also find combining different modelling approaches provides the best forecasts for these profit series.

Our NIPA models place greater weight on changes in nominal GDP, whereas our S&P 500 earnings models stress real GDP growth. This is because NIPA profits peak earlier in the cycle as growth and inflation start to decline, while S&P 500 earnings stay strong for longer as growth can remain positive very late in the cycle.

This disparity is evident in the below chart, where we see a gap between the S&P 500’s earnings per share (EPS) and the operating profits of the overall US economy consistently open up before recessions over the past 30 years.

This discrepancy is usually only resolved when the economy enters a recession and businesses recognise write downs and capital losses.

This means that an earnings recession would be likely to first become visible in the NIPA data, but regardless of the approach we take the indicators point toward a severe drop in profits if the Fed fails to achieve a soft landing.

In short: the softer landing the Fed can engineer, the better.

Our forecasts anticipate the US economy continuing to expand for the next few quarters, with inflation moderating but remaining well above target. This combination should lead to strong growth in revenues, which in turn should keep earnings growing despite the headwinds they face from high input costs.

Eventually, we expect the Fed to succeed in pushing down both GDP growth and inflation, but as this occurs real unit labour costs would stay high until unemployment has risen significantly.

In our models of this scenario, continuing wage growth would closely correlate with falling profits. These could work in tandem with stalling GDP growth to potentially put severe pressure on earnings growth at some stage next year.

However, this is not set in stone. There are several key questions that will determine profits’ trajectory.

Will wage growth ease as nominal sales fall? Is the momentum behind this growth partly or mostly attributable to re-opening? And will a significant increase in the labour supply be sufficient to slow wage growth?

Beyond these variables, the composition of broader GDP growth has its role to play.

We have some concerns that the rotation from goods to services could dampen earnings, but this could potentially be offset by an improving global backdrop. The present energy shock as a result of the war in Ukraine is more keenly felt in Europe and emerging markets than the US, and there is some chance it may ease during 2023 – making for a more beneficial growth environment in these regions.

This leads us to believe the S&P 500’s earnings are likely to be more resilient than those of the broader US market, as has often been the case in late-cycle environments. This is because the large-caps that make up that index tend to be both less exposed to drag from labour cost pressures and more regionally diversified, benefiting from the stronger economies we forecast across Europe and global emerging markets.

At present, the risks to earnings we see emerging beyond the next 12 months are too distant and therefore too uncertain to drive returns and turn us bearish.

Meanwhile, innovative technologies and creative management practices could both unlock productivity gains and reduce unit labour costs – although the impacts of these are of course hard to predict.

[1] https://www.marketwatch.com/story/u-s-corporate-profits-jump-25-in-2021-as-economy-rebounds-from-pandemic-11648644379

Disclaimer: Views in this blog do not promote, and are not directly connected to any Legal & General Investment Management (LGIM) product or service. Views are from a range of LGIM investment professionals and do not necessarily reflect the views of LGIM. For investment professionals only.